September 8, 2022

LETTER AS A CONCERNED STAKEHOLDER OF

QUANTUM COMPUTING INC.

QUANTUM COMPUTING INC.

Dear Members of the Board and Shareholders:

BV Advisory Partners, LLC (together with its affiliates, “BVP” or “we”)* are stakeholders** of Quantum Computing, Inc. (Nasdaq: QUBT) (the “Company” or “QUBT”).

* BVP was a [financial advisor] to QPhoton, Inc., a Delaware company, (“QPhoton “) who was acquired by QUBT on June 16, 2022 in a merger (the “Merger”) pursuant to an Agreement and Plan of Merger, dated May 18, 2022 by and among, QUBT, two of its wholly-owned subsidiaries, QPhoton and Yuping Huang, the former Chairman. Chief Executive Officer, President and, together with his wife, Xiao Pan, who also was a QPhoton director, the holder of more than 80% of the outstanding QPhoton common stock; and since the Merger closing has been the Chief Quantum Officer, a director and the largest shareholder of QUBT. BVP also was a 10% stockholder of QPhoton, introduced and arranged the license by QPhoton of all of its quantum intellectual property from the Stevens Institute, provided the initial $500,000 of funding to QPhoton through the purchase of $500,000 QPhoton convertible notes (the “Notes”), assisting in the building of QPhoton into an operational company, and introduced QPhoton to QUBT. Because BVP did not receive any cash compensation for its 18 months of services to QPhoton and for the risks taken by BVP in providing the $500,000 of initial financing to QPhoton, at a time when QPhoton had no funds, revenues and/or any other prospects or sources of funding, QPhoton agreed in the Notes and the Note Purchase Agreement with BVP dated March 1, 2021 (the “NPA”) that upon the closing of the Merger (a change of control), BVP would receive as payment for its Notes a dollar amount equal to the market value of the number of shares of QUBT common stock BVP would receive as if it converted its Notes into QPhoton common stock, as adjusted based upon an arms-length negotiated formula between QPhoton and BVP including as to the conversion price, immediately prior to the Merger, which payment amount as of the date of Merger closing was $13,182,140 million. Because BVP believes QPhoton and QUBT breached their payment obligations under the Notes and the NPA, on August 15, 2022, BVP sued QPhoton, QUBT and its executive officers Robert Liscouski, CEO and Director, William McGann, COO and CTO and Chris Roberts CFO as well as Greg Osborne, the Director of Business Development of QUBT, Joseph Salvani, who BVP believes based upon, among other factors, correspondences with QUBT and representations by Salvani and others, that Salvani is an undisclosed “founder,” principal and control person of QUBT, and Dan Walsh, identified in QUBT correspondence to BVP as Salvani’s “partner (cap markets).” In prior actions brought by the SEC against Salvani, Osborne, such persons were sanctioned by the SEC for violations of the United States Federal Securities Laws. See https://www.sec.gov/litigation/admin/34-44590.htm (cited as: Joseph

M. Salvani, Exchange Act Release No. 44590 (July 26, 2001)) and https://www.sec.gov/litigation/opinions/2019/33-10641.pdf (cited as: Gregory Osborn, Securities Act Release No. 10641, Exchange Act Release No. 86001, Investment Company Act Release No. 33498, 2019 WL 2324337 (May 31, 2019)). BVP’s Verified Complaint, captioned, BV Advisory Partners, LLC, (Plaintiff) v. Quantum Computing Inc., QPhoton, LLC, Yuping Huang, Xiao Pan, Robert Liscouski, William McGann, Chris Roberts, Joseph Michael Salvani, Gregory Osborn, and Dan Walsh, (Defendants), C.A. No. 2022-0719-SG (Del. Ch. filed on Aug. 15, 2022). A copy of the complaint is attached hereto as Exhibit A.

** Because of BVP’s concerns regarding and the actions of QUBT including its management and the QUBT Board as set forth in this letter and in BVP’s litigation complaint, BV has demanded its appraisal rights with regard to its QPhoton demanded.

We write to identify several troubling issues raised by QUBT’s disclosures and SEC filings, including in QUBT’s recent Stockholder Letter, Quarterly Report on Form 10-Q for the quarter ended June 30, 2022, its Definitive Proxy Statement and Annual Report for its September 21, 2022 Annual Meeting of QUBT Stockholders (the “2022 QUBT Proxy/Annual Report”) and various other QUBT SEC filings. All of QUBT’s SEC filings and Reports, including the above, are available for review under “Quantum Computing, Inc.” on the SEC’s EDGAR database, available at https://www.sec.gov/edgar/search-and-access.

We also write to suggest that the following steps be immediately taken: to preserve the Company and shareholder value, including by:

- Delaying the September 21, 2022 Stockholder meeting until the pending “Delaware Lawsuit” ferrets out the truth of QUBT management and directors’ self-dealing;

- Rejecting QUBT management’s request for shareholders to approve larger, more lavish compensation for management at that September 21, 2022 Stockholder meeting;

- Prohibiting QUBT management and QUBT Board members from engaging in and/or approving any transactions with QUBT, given their history of self-dealing; and

- Immediately establishing an independent committee with all authority and means necessary to investigate all QUBT management and QUBT Board members relationships and self-dealing, including their relationships with the Toxic Micro-Cap Network Affiliates described below.

Moratorium on Toxic Dilutive Equity Offerings and Delay of Shareholder Meeting

As a concerned stakeholders, we believe it is important to communicate to the entire QUBT Board concerns that we and other stockholders have expressed via message boards regarding QUBT. Because of the Company’s November 21, 2021 dilutive and toxic Preferred Stock offering and the history of various certain QUBT’s officers, directors in the micro-cap securities and their relationships and involvement with funding entities in such industry, there is a strong concern that the QUBT Board may engage in further destructive and dilutive offerings without independent shareholders’ consent. We are particularly concerned that QUBT’s management has asked its stockholders to approve lavish new compensation packages for QUBT management at the September 21, 2022 Annual QUBT stockholder meeting, despite the fact that QUBT’s cash reserves are rapidly dwindling: [In QUBT’s June 30, 2022 10-Q, QUBT disclosed that as of July 31, 2022, it had cash on hand of approximately $5.9mm, which was down (i) $10.8mm from the approximately $16.7mm of cash at January 1, 2022, and (ii) $9.2mm from the approximately

$15.1mm of cash at 3/31/2022,] but only generated approximately $96,000 in revenue, (which mostly resulted from related party transactions). We believe that the current compensation public to QUBT management is unsustainable and that approving QUBT management’s compensation proposals would be particularly reckless because QUBT management has failed to articulate a sound business model that could be implemented by an experienced technology management team—which QUBT lacks; and has failed to provide a clear, detailed, measurable, and understandable path to sustainable profitability.

QUBT’s current head of sales has a total compensation package of over $500,000 per year, which is outrageous for many reasons including his lack of quantum technology experience, and QUBT’s non-existent commercial products, revenue run-rate and substantial operating and net losses. In a previous conference call in December 2021, we asked him to provide details on his sales and revenue pipeline projects but he could not provide an answer, but instead said his projections were a “SWAG”. This compensation approach is irresponsible and not aligned in any way with the best interest of shareholders.

In fact, the majority of QUBT’s revenue was generated from an affiliated company MMMM that Robert Liscouski also serves on that board of directors. Further toxic dilutive securities offerings by the QUBT Board would clearly be contrary to the best interests of shareholders. Therefore, I am requesting the QUBT Board delay its September 21, 2022 Stockholder meeting until the resolution of the pending BVP lawsuit in Delaware, and that the current management team can demonstrate their ability to follow good corporate governance procedures and the expertise to grow a quantum computing company. To be clear, given the Company’s history of underperformance [and poor corporate governance, in burning cash on officers and directors compensation with very little revenue generated we believe that the QUBT Board should refrain from engaging in any transactions including those set forth in QUBT’s 2022 Proxy/Annual Report with its executives, QUBT Board members, affiliates and/or related parties, including employment, consulting advisory and/or other contracts and agreements and increases in or providing additional compensation as well as any issuances and/or sales dilutive and/or toxic financings including involving convertible notes, debt or stock until the pending BVP litigation is resolved.

Misaligned Board Representation

BVP believes that the Quantum computing industry is an exciting technology and is at an important inflection point. Although as a result of its acquisition of QPhoton, QUBT now appears to have potential groundbreaking technology that could solve business problems, the Quantum computing industry has larger better-funded and better managed competition. Quantum computing competition includes companies such as Google, IBM, IONQ, D-Wave and Righetti all of whom have significantly more capital either from their own cash balance or equity raised from leading venture capital and institutional investors than QUBT to fund their Quantum platform and technology. In addition, QUBT’s competition has leading technology experts as board members and technology advisors. We believe the QUBT Board needs to have better technology industry experts to advise it on, among other items, strategy and management execution. BVP has identified a number of independent board candidates with significant technology expertise who can advise on strategy, business plan implementation and relationships within the technology and business community. In addition, we are concerned that the prior owners of QPhoton own 49% of QUBT equity, but QUBT has nominated just one Q-Photon representative despite the contractual right of Mr. Huang to appoint 3 new QUBT Board members. This action is inexplicable and defies common sense.

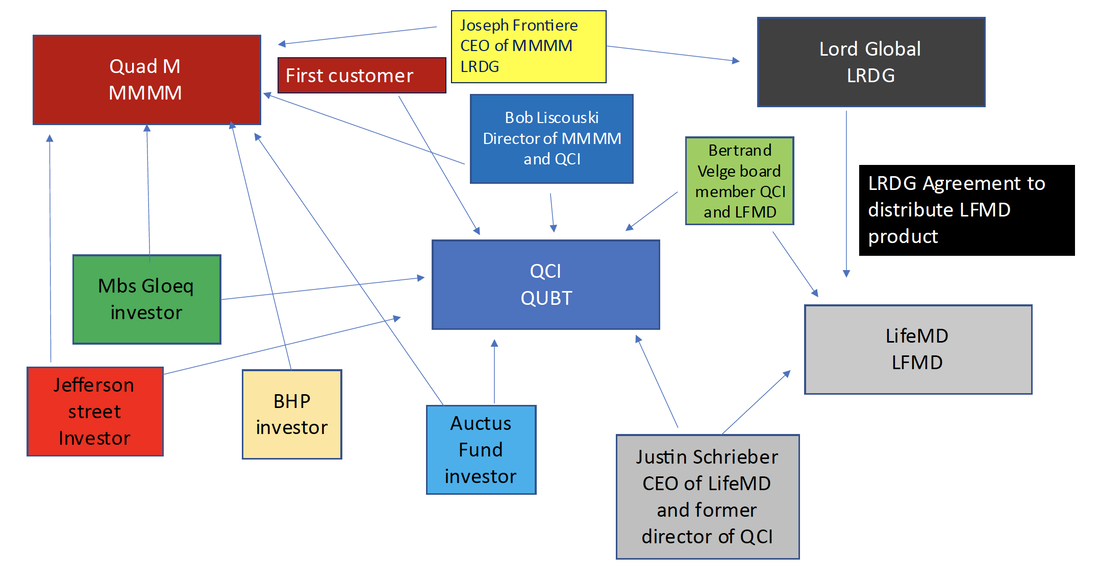

Toxic Micro-cap network Affiliation

All shareholders of QUBT should also be quite concerned of the cash burn on compensation with very little revenue, and about the inter-party network of relationships between QUBT and members of the “toxic penny stock network”. We believe that the equity market capitalization value of a public company that is associated with this type of network will be severely negatively affected. Potential strategic and institutional investors will likely avoid investing in any public company that has the taint of a “toxic penny stock,”

See the below Diagram below that highlights the “network” QUBT is associated with.

We believe it is imperative that the QUBT Board immediately end all QUBT associations with this network by changing the current QUBT management team and QUBT Board composition as well as terminating other relationships and associations involving the toxic network. In addition, we believe QUBT’s current CEO as a board member of Quad M Solutions, Inc. (OTC: MMMM) is exposing QUBT to reputational risk. Quad M repeatedly files with the SEC notices of inability to make timely filings of reports as required to be made by it with the SEC, and the same individual serving the CEO, CFO and chief accounting officer of Quad M is also the CEO of at least two other micro-cap companies (LRDG, and GXXM). On August 20, 2020 the SEC issued an order of Suspension of Trading on (LRDG) for making false statements to the public. QUBT recent SEC filing appears to have been late, and it’s our concern that late SEC filings is a dangerous pattern. The QUBT CEO’s decision to be on the board of a publicly company with questionable corporate governance suggests poor judgement and any association with this type of network has the potential to hurt the value of QUBT shares thereby negatively affecting all QUBT shareholders. It’s our belief the independent members of the QUBT Board should immediately establish a committee, with the authorization to retain necessary experienced and independent legal counsel and other independent professionals to investigate and evaluate all QUBT director and executive relationships with this network and in related party transactions and share the findings of this exercise with all shareholders.

Lack of Management Credibility

Management has indicated that shareholders would see returns on QUBT’s investments in the form of accelerated revenue growth, but that appears not to be the case. It appears that neither the CEO of QUBT, nor the QUBT Board has upheld their fiduciary duties: instead, they have burned through substantial amounts of QUBT’s cash on excessive salaries without showing tangible results for the spent funds and engaging in toxic financings orchestrated by a person who has been sanctioned by the SEC for acting as an unregistered broker/dealer in violation of the United State Federal Securities Laws. If QUBT management and/or the QUBT Board did any basic diligence (or paid attention to any reasonable due diligence performed) prior to the November 2021 toxic financing, they would have seen the disastrous death spiral outcomes that followed.

Summary

BVP strongly believes that it should be allowed to appoint its own slate of board representatives independent of QUBT management. QUBT should end all association with Mr. Osborne, Salvani and Walsh. BVP slate of board representatives should be immediately added to the QUBT Board to ensure that decisions are made with the best interests of all stakeholders and to protect the solvency, assets and governance of QUBT. We call on the independent members of the QUBT Board to immediately form an independent committee with the authority to retain and pay independent and experienced legal counsel and other professionals to investigate and publicly report the concerns set forth in this letter and related matters including QUBT management. We look forward to a constructive engagement with the QUBT Board and working with the QUBT Board to fully explore all opportunities available to maximize shareholder value.

Sincerely,

Lack of Management Credibility

Management has indicated that shareholders would see returns on QUBT’s investments in the form of accelerated revenue growth, but that appears not to be the case. It appears that neither the CEO of QUBT, nor the QUBT Board has upheld their fiduciary duties: instead, they have burned through substantial amounts of QUBT’s cash on excessive salaries without showing tangible results for the spent funds and engaging in toxic financings orchestrated by a person who has been sanctioned by the SEC for acting as an unregistered broker/dealer in violation of the United State Federal Securities Laws. If QUBT management and/or the QUBT Board did any basic diligence (or paid attention to any reasonable due diligence performed) prior to the November 2021 toxic financing, they would have seen the disastrous death spiral outcomes that followed.

Summary

BVP strongly believes that it should be allowed to appoint its own slate of board representatives independent of QUBT management. QUBT should end all association with Mr. Osborne, Salvani and Walsh. BVP slate of board representatives should be immediately added to the QUBT Board to ensure that decisions are made with the best interests of all stakeholders and to protect the solvency, assets and governance of QUBT. We call on the independent members of the QUBT Board to immediately form an independent committee with the authority to retain and pay independent and experienced legal counsel and other professionals to investigate and publicly report the concerns set forth in this letter and related matters including QUBT management. We look forward to a constructive engagement with the QUBT Board and working with the QUBT Board to fully explore all opportunities available to maximize shareholder value.

Sincerely,

Keith Barksdale

Managing Member

BV Advisory Partners, LLC

Managing Member

BV Advisory Partners, LLC